Editor: Crass Cash

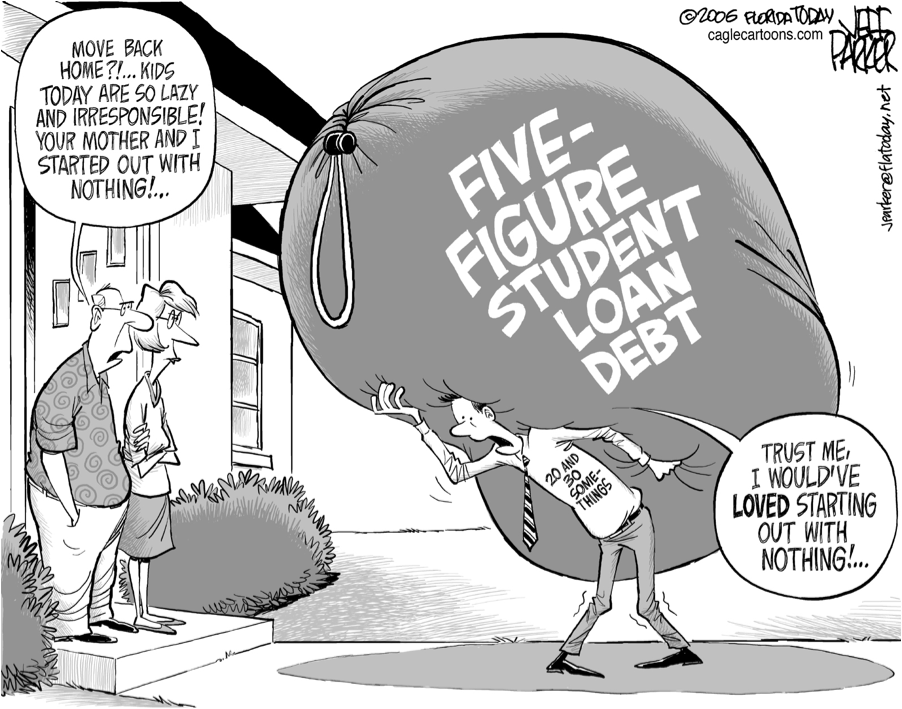

Ah student loans. The misunderstood and bane of existence for recent grads. Although people are putting this off more and more it's now becoming a problem for the middle aged population as well. So what can you do about it? Here are a number of tips to help you conquer this!

1. Don't put off or defer the payments. This will end up costing you big time later on. Deferring them is even worse then the "minimum payment" on your credit card. Always pay something! Even if it's a very small amount. The whole idea is that you recognize it in your brain each month and focus on it. Putting it aside while you go out for a beer hurts you immeasurably later on due to compound interest.

2. Get a roommate! Live that college lifestyle until it's paid off. As long as you have a student loan, still consider yourself to be in college. The couple hundred bucks that you could save by living like you're still in college will allow for you to at least half the time that it'll take to pay it off.

3. Throw everything at it, plus the kitchen sink! Make extra payments towards the principle. This is like compound interest in retirement, but in reverse since it's paying off debt. I've seen people who have had the money to pay off their student loans, but instead had their cash since in a bank account making .01% interest while they're paying 6% interest on the loan. Stupid!

4. Work extra side jobs for cash. Learn how to bar tend on the weeks or bust tables. Even if it's just $25 for a few hours of work. Put all of it towards your loan. By throwing a measly $100 more at the loan each month, you'll reduce a $20,000 loan from 20 years to 8 years and 11 months. More than half!

5. Take the job that nets you the most money, not the most that you'll make. We all want to live in bitchin' ass cities where the ladies are sowing their wild oats and getting drunk at trendy bars (remember you're just out of college). But taking that job in Boston, NYC, LA or Chicago doesn't mean that you're going to save as much vs taking on in say Tampa, Austin, or Nashville. You can easily save more money in those cities due to the low cost of living vs the former. As a result you can retire that debt in a quarter of the time. Remember how much $100 a month lowered your student debt by? Now imagine if you throw thousands a year at it vs $1,200.

6. Loan forgiveness. For those of you who are looking to go into the following fields: military, public safety, public health, education, and law for the govt. You may be eligible to have all of your student loans forgiven after 10 years. Assuming that you've made full on time payments the whole time.

7. Quit saying that student loan interest saves you money. Yes it is possible to save some money on your taxes due to student loan interest. Up to $2,500 as a matter of fact. But chances are you're not going to get nearly that much or anything at all. You need to meet these 5 qualifications.

If you're making more than $75,000 in MAGI as an individual, then you're not going to get any sort of benefit from this. If you make less than $60,000 than you'll get full benefit. If you make in between than your deduction will get phased out. If you're one of the lucky ones who gets a deduction, then TAKE ALL OF THE SAVINGS AND PUT IT TOWARDS THE DEBT!

8. Quit bitching. That's right, the average student loan is almost he equivalent to the average car loan. That car loan you'll probably pay off in 5 years if you're seriously slacking, so quit bitching. Put on your big girl pants and start paying it off early. Waiting around for President Obama to wave a magic money wand to make it all go away isn't going to happen. Suck it up and pay it off!

1. Don't put off or defer the payments. This will end up costing you big time later on. Deferring them is even worse then the "minimum payment" on your credit card. Always pay something! Even if it's a very small amount. The whole idea is that you recognize it in your brain each month and focus on it. Putting it aside while you go out for a beer hurts you immeasurably later on due to compound interest.

2. Get a roommate! Live that college lifestyle until it's paid off. As long as you have a student loan, still consider yourself to be in college. The couple hundred bucks that you could save by living like you're still in college will allow for you to at least half the time that it'll take to pay it off.

3. Throw everything at it, plus the kitchen sink! Make extra payments towards the principle. This is like compound interest in retirement, but in reverse since it's paying off debt. I've seen people who have had the money to pay off their student loans, but instead had their cash since in a bank account making .01% interest while they're paying 6% interest on the loan. Stupid!

4. Work extra side jobs for cash. Learn how to bar tend on the weeks or bust tables. Even if it's just $25 for a few hours of work. Put all of it towards your loan. By throwing a measly $100 more at the loan each month, you'll reduce a $20,000 loan from 20 years to 8 years and 11 months. More than half!

5. Take the job that nets you the most money, not the most that you'll make. We all want to live in bitchin' ass cities where the ladies are sowing their wild oats and getting drunk at trendy bars (remember you're just out of college). But taking that job in Boston, NYC, LA or Chicago doesn't mean that you're going to save as much vs taking on in say Tampa, Austin, or Nashville. You can easily save more money in those cities due to the low cost of living vs the former. As a result you can retire that debt in a quarter of the time. Remember how much $100 a month lowered your student debt by? Now imagine if you throw thousands a year at it vs $1,200.

6. Loan forgiveness. For those of you who are looking to go into the following fields: military, public safety, public health, education, and law for the govt. You may be eligible to have all of your student loans forgiven after 10 years. Assuming that you've made full on time payments the whole time.

7. Quit saying that student loan interest saves you money. Yes it is possible to save some money on your taxes due to student loan interest. Up to $2,500 as a matter of fact. But chances are you're not going to get nearly that much or anything at all. You need to meet these 5 qualifications.

- You paid interest on a qualified student loan in tax year 2013

- You are legally obligated to pay interest on a qualified student loan

- Your filing status is not married filing separately

- Your modified adjusted gross income is less than a specified amount which is set annually, and

- You and your spouse, if filing jointly, cannot be claimed as dependents on someone else's return

If you're making more than $75,000 in MAGI as an individual, then you're not going to get any sort of benefit from this. If you make less than $60,000 than you'll get full benefit. If you make in between than your deduction will get phased out. If you're one of the lucky ones who gets a deduction, then TAKE ALL OF THE SAVINGS AND PUT IT TOWARDS THE DEBT!

8. Quit bitching. That's right, the average student loan is almost he equivalent to the average car loan. That car loan you'll probably pay off in 5 years if you're seriously slacking, so quit bitching. Put on your big girl pants and start paying it off early. Waiting around for President Obama to wave a magic money wand to make it all go away isn't going to happen. Suck it up and pay it off!

RSS Feed

RSS Feed